The global energy storage market is set to grow significantly by 2030 despite a short-term drop in deployments due to the coronavirus pandemic.

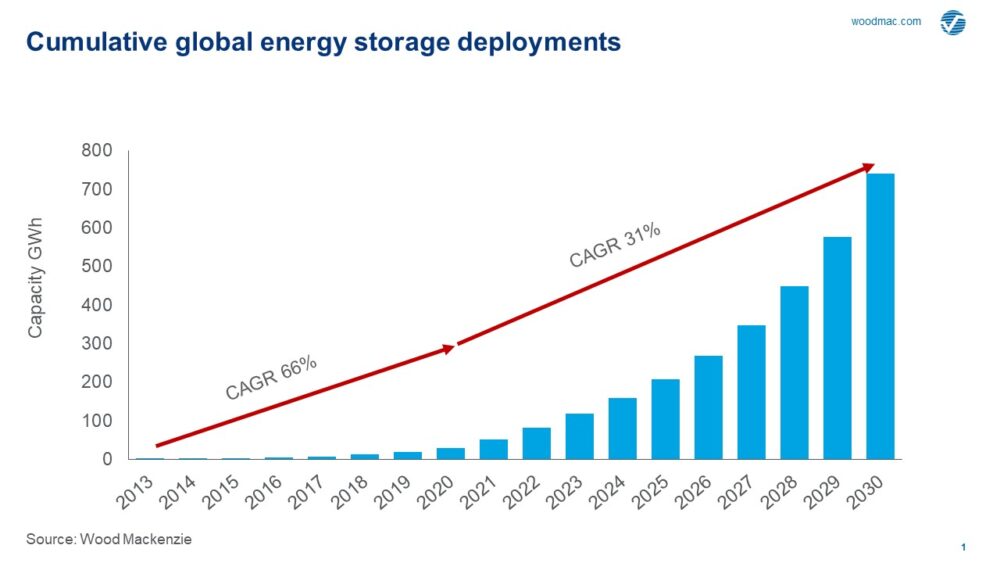

That is according to the latest report by energy researcher Wood Mackenzie, which shows the storage market will increase by a compound annual growth rate (CAGR) of 31%, recording 741 gigawatt-hours (GWh) of cumulative capacityby the end of the decade.

Front-of-the-meter (FTM) will continue to dominate annual deployments and will account for up to 70% of annual total capacity additions up until 2030.

Wood Mackenzie’s principal analyst Rory McCarthy said: “We note a 17% decrease in deployments in 2020, 2 GWh less than our pre-coronavirus outlook.

“We expect wavering growth in the early 2020s, but growth will likely accelerate in the late 2020s, to enable increased variable renewable penetration and the power market transition.”

Stakeholders are continuing to invest in the global energy storage market

Wood Mackenzie still considers energy storage as a nascent market, as it has a relatively new investment class with underlying risks.

But it believes the stakeholders – whether end-consumers or big equity investors – are interested in continuing to invest in the sector and do not appear to be hindered by the pandemic and economic recession impacts.

McCarthy said: “Investment decisions are likely to be pushed back in some cases, but the general trajectory of the power market transition and the need for energy storage to enable this has not changed.

“If anything, the transition may be accelerated as governments around the world grapple with how to recover their economies more sustainably than in the past with upside for the energy storage industry.”

The US will continue to lead the way in capacity up until 2030

The US maintains its pole position and will make up more than 49% or 365 GWh of global cumulative capacity by 2030.

The report notes that utility resource planning in the US is set to take a “front seat for deployments” over the coming decade.

It added that across the past two years, utility approaches to renewables and particularly storage have “shifted seismically”, with the majority of utilities “dramatically shifting” planned resources towards renewables and storage due to cost and state-driven clean-energy goals.

As a result, Wood Mackenzie expects the US FTM marketto surge during 2021 due to significant short-term resources it has in the pipeline, before then slowing slightly through to 2025.

Beyond 2025, it believes growth will “become steadier” as wholesale market revenue streams grow and utility investment is normalised.

The market will reach a CAGR of 36% over the coming decade, with cumulative capacity installed approaching 300 GWh, according to the report.

It predicts China, coming in second after the US, will see its cumulative storage capacity “grow exponentially” – accounting for 21% or 153 GWh of global cumulative capacity by the end of the decade.

Wood Mackenzie said the ancillary service market is the primary revenue stream for the FTM market and will continue to attract hybrid storage installations in China from 2020 to 2025.

It highlights firming renewables capacity to reduce curtailments as the second-most important driver in Australia, China, South Korea and Japan.

According to the analysis, China launched a policy that requires solar and wind developers to make up the costs for building stable and grid-friendly renewable generation assets.

It said energy arbitrage will make up the additional revenues for storage as more Asia Pacific power markets may be “fully liberalised” from 2025 to 2030.

Europe will experience slow growth in the energy storage market

Wood Mackenzie expects Europe’s growth story to be “slower than its global counterparts”.

The UK and Germany will continue to dominate the FTM market up until 2025, while frequency response auctions will remain one of the “key revenue streams”.

France and Italy are also opening up with both capacity and ancillary service markets open or opening. The report anticipates Spain, and the rest of continental Europe to follow that pattern, with potential help from the European Commission and its green recovery deal.

Wood Mackenzie’s senior analyst Le Xu believes storage “holds the key to strong renewables growth”.

“The question is whether storage can capture stable long-term revenue streams,” she added.

“Low-cost and longer duration storage can increasingly out-compete coal, gas and pumped hydro, enabling higher levels of solar and wind penetration.

“However, most lithium-ion energy storage systems economically max out at four to six hours, leaving a gap in the market.”

The report notes that the future of storage will require safe, low-cost batteries, with battery manufacturing splitting between stationary and EV batteries due to “differing needs cases”.

It anticipates LFP (lithium iron phosphate) to overtake NMC (nickel manganese cobalt) as the dominant stationary storage chemistry within the decade, growing from 10% of the market in 2015 to more than 30% by 2030.