The investment gap between renewable energy projects and upstream oil and gas is narrowing, as the low-carbon transition gathers momentum and the oil industry tightens its purse strings after a loss-making 2020.

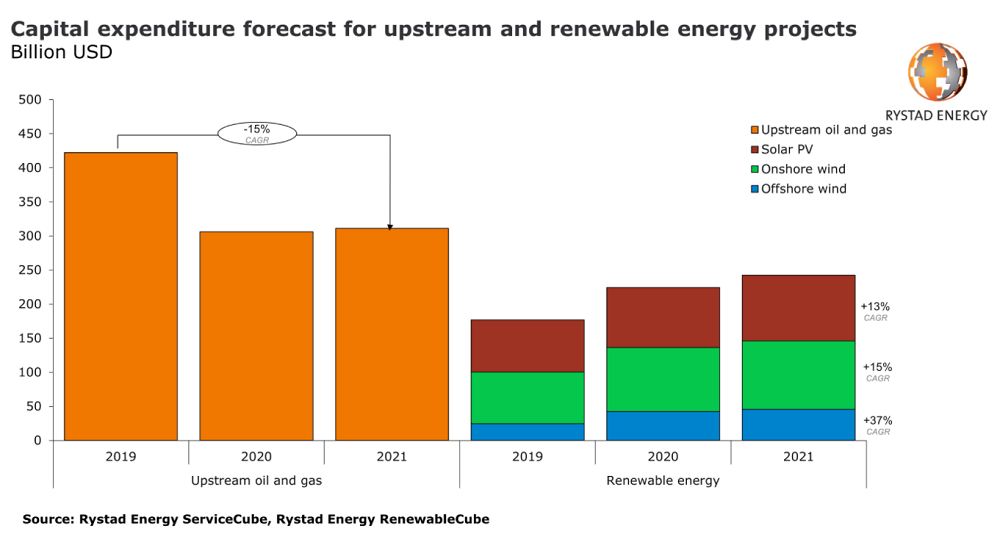

According to research group Rystad Energy, capital outlay on renewables will reach a record $243bn this year – up from $224bn in 2020 and edging closer towards expected oil and gas spending of around $311bn.

Onshore wind projects account for the bulk of these investments at roughly $100bn, while solar PV will receive $96bn and offshore wind around $46bn.

Asia and Europe will dominate these transactions, with 156 gigawatts (GW) and 32 GW of capacity under construction at the start of the year respectively. A trio of wind developments – China’s Rudong and Zhuozi County wind farms, and the UK’s Hornsea 2 project – will be major drivers of spending throughout the year.

Growing investment in renewable energy projects could prompt service providers to switch focus

For energy service providers, the shifting trend in capital allocation could demand a reconsideration of their core business focus, as green projects continue their ascendency and fossil-facing exploration and production activities are limited by capital discipline.

The pandemic delivered a huge financial shock to oil companies in particular as demand for their products fell away during lockdowns – prompting a major scaling back of medium-term investment plans across the industry.

According to the International Energy Agency (IEA), this disruption caused a 30% decline in global oil and gas spending last year, and investments are expected to rise “only marginally” this year. Over the medium-term, the agency says spending among the majors is expected to stay roughly 15% below 2019 levels.

“Demand destruction, and its uncertain recovery due to Covid-19, continues to have a dramatic impact on upstream investment,” the IEA said in its latest oil market report.

Renewables meanwhile proved much more resilient during the crisis as companies pushed ahead with their low-carbon transition plans, particularly with a view to meeting subsidy and tax incentive deadlines in key markets.

Rystad’s energy service analyst Chinmayi Teggi said: “Last year’s events forced leading oil and gas businesses to look at strategies to reduce exposure to the risky market amid the energy transition.

“Oilfield service suppliers, for instance, have started a considerable transformation, hoping to be more relevant in a greener market and become a more attractive option for investors.”

Analysis from the consultancy shows that energy service suppliers exposed to upstream oil and gas sectors saw revenues drop by 23% in 2020, compared to the previous year, while those with a focus on wind and solar saw sales grow by around 18%.

Looking more closely at the fourth quarter of 2020, Rystad notes that upstream-focused service providers suffered a 25% year-on-year revenue decline “amid a lack of new contracts and slow execution of backlog work”.

Revenue from well services and seismic segments fell last year by 35% from 2019 levels, while drilling tools revenue shrank 25%, it added.

Meanwhile, “service players exposed to wind projects recorded a 15% year-on-year boost to revenues for the fourth quarter of 2020, with full-year revenues improving by 20%. Sales at service providers exposed to solar projects rose 3% in the fourth quarter from the year-earlier period and climbed 14% for the full year.”