The Energy Bill introduced to the UK parliament in January 2008 cites two long-term energy challenges faced by the UK: tackling climate change by reducing carbon dioxide emissions, and ensuring secure, clean and affordable energy. Concern about climate change remains at the heart of UK energy policy and, in everyday life, carbon footprints are a growing preoccupation.

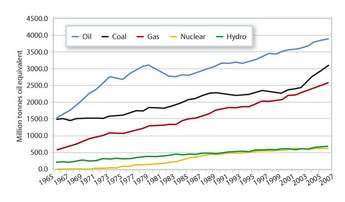

Meanwhile, the world at large continues to demonstrate its insatiable appetite for fossil fuels in general, and coal in particular. Since 2003, coal has been the fastest growing fossil fuel, and in 2006 consumption was 3.1 billion tonnes oil equivalent, almost 30% above the 2001 level. Unlike oil and gas, most of the world’s coal is consumed in the country where it is produced, with only around 15% traded internationally.

The fastest growth of all has been in China, which now accounts for almost half of world coal production. In 2006, the growth in Chinese output was 322 million tonnes – more than total UK consumption for the past five years.

This is not perversity in the face of international concern, but pragmatism in recognition of reality. China’s proven coal reserves are 167 billion tonnes (Reserves, Resources and Availability of Energy Resources 2006. Bundesanstalt für Geowissenschaften und Rohstoffe (Federal Institute for Geosciences and Natural Resources)) equivalent to over 60 years supply at current rates of consumption. Estimated additional coal resources, yet to be accurately assessed and defined, are a massive 4.2 trillion tonnes. China’s total coal resources represent 46% of the global total compared with 2% for oil and 3% for gas. Given these quantities, it is inconceivable that China will not use its coal to fuel the growth of its economy.

China is not unique in this respect, except by virtue of its sheer scale. Coal resources are widely accessible, unlike oil and gas, and they will inevitably be used as an engine of growth. India has proven reserves of 95 billion tonnes and Russia of 70 billion tonnes. The USA has the world’s largest proven coal reserves, of 213 billion tonnes, and it is clear that it intends to use them.

Against this background it is futile to pretend that global CO2 emissions can be capped, or reduced, through renewables and energy saving alone. Wealthy countries are most able to afford the more expensive routes to climate change mitigation, but with 1.6 billion people in the world still without access to electricity, and with a thirst for improved lifestyles in developing economies, many of these technologies look like just another Western luxury.

Whilst clean coal with carbon capture and storage (CCS) may not be a silver bullet, it is likely to be an essential tool in carbon reduction. This is recognised by governments and institutions concerned to find solutions to climate change. In its 2006 Energy Package, the European Commission said ‘While the transition from traditional coal to Sustainable Coal will certainly not be costless, it may prove a priceless contribution to climate change mitigation’. The World Wildlife Fund, not generally seen as a friend of coal, cites CCS as one of six key solutions to global warming.

In the UK, ministers, politicians and government officials also speak enthusiastically about CCS. But how can they expect China or India to take seriously our intentions when the UK is only planning to demonstrate CCS on 300 MW of electricity generation capacity by 2014 – less capacity than China builds every week? This is merely scratching the surface. The UK has a unique set of circumstances to lead the way in CCS: a need for new generation capacity; good access to storage under the North Sea bed; many companies wishing to pursue projects; and an economy strong enough to support the development.

These projects will not go ahead without a lead from government. The costs and risks of the pathfinding projects will need direct support or market mechanisms – as do renewable technologies and other low carbon solutions. The government has a choice – either to show global leadership in making coal a part of the solution to climate change or to stand back. Standing back may simply allow others to take that lead; or worse, it may involve watching unabated use of coal continue to power global growth while we salve our conscience, pursuing other technologies which have less global reach.