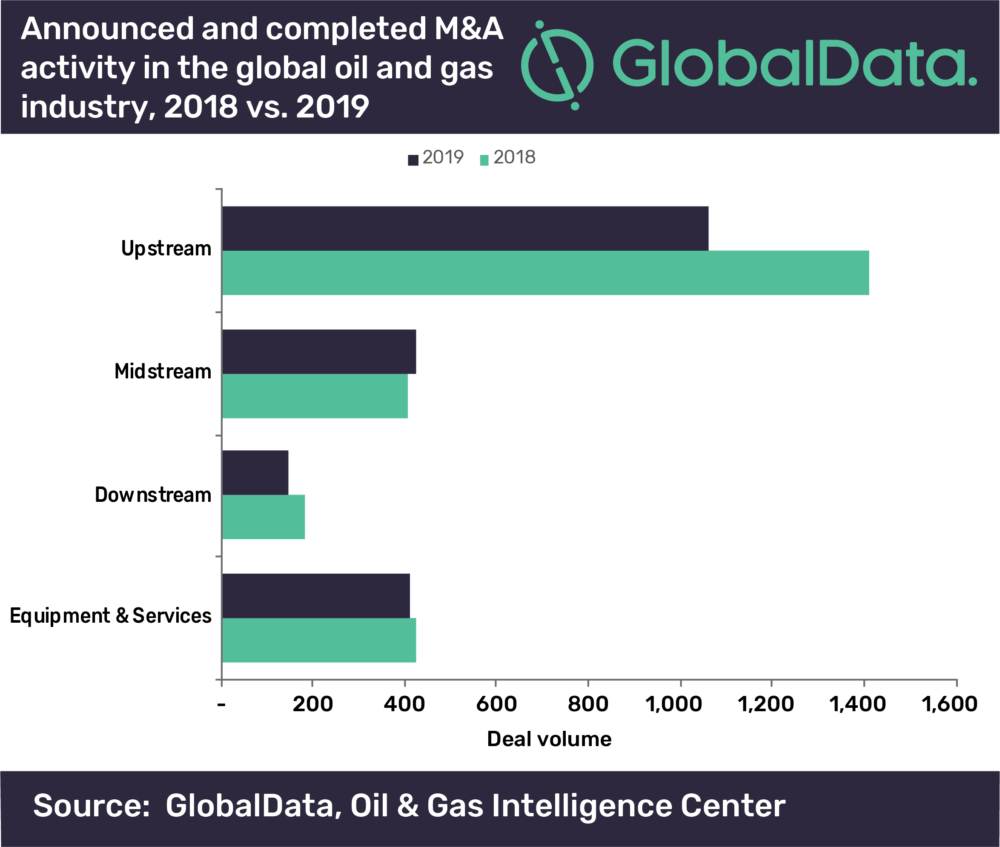

The upstream sector experienced the most oil and gas mergers and acquisitions (M&A) in 2019, says an analyst.

Occidental Petroleum’s $57bn purchase consideration of fellow Texas-based company Anadarko Petroleum was the biggest M&A deal in the sector last year.

A report by data and analytics firm GlobalData found deals largely revolved around the need to improve company finances and reduce debt.

GlobalData oil and gas analyst Ravindra Puranik said the upstream sector witnessed the most activity because of investments in US shale plays, which are rapidly developing into available sources of natural gas.

“The leaseholds in Delaware and Midland Basins of Texas and New Mexico were among the most sought after assets in the US, largely down to their proximity to the refining and petrochemical complexes along the Gulf of Mexico,” he added.

“In fact, the vast acreage held by Anadarko Petroleum in the Permian Basin was the main reason behind its acquisition by Occidental Petroleum to mark the biggest deal of last year.

“Oil and gas companies also acquired assets in the gas-rich Appalachia Basin as it serves key commercial centres on the US East Coast.”

Upstream oil and gas mergers and acquisitions led the way in 2019

Alongside the US shale resources, oil sands deposits in Alberta and Saskatchewan in Canada also featured in deal activity in 2019.

This was because companies, especially non-Canadian firms, divested their assets to Canadian operators amid infrastructure and environmental concerns.

Oklahoma-headquartered Devon Energy sold its oil sands assets to Canadian Natural Resources to focus on operations in the US.

Puranik said divestment was also the reason for deal activity in other regions, such as the North Sea, the Caspian Sea, and the Australian upstream sector, as oil and gas multinationals embarked on ways to optimise their portfolio.

“This was led by ConocoPhillips and Chevron, while other companies, including BP, ExxonMobil, and Shell followed suit,” he added.

“More divestments are expected from oil majors in 2020 as oil and gas prices are anticipated to remain low in the near future.”

Midstream and downstream sectors also witnessed notable deals last year, particularly for pipeline assets in key oil and gas producing regions around the world — with Petrobras, Marathon Petroleum, Saudi Aramco, and Total among the companies executing high-value deals.

Petrobras, the Brazilian national oil company, divested its midstream assets to an international consortium for $8.6bn.

Puranik said following pressure from the government to reduce debt and cut down its monopoly on the country’s oil and gas industry, the company is also evaluating a proposal to trim its downstream business.

Oil and gas firms placed emphasis on maintaining capital discipline for mergers and acquisitions

As companies focused on improving their finances and reducing debt, this drove multinational oil and gas majors, such as ExxonMobil, ConocoPhillips, and Chevron, to review their global operations and begin divesting non-profitable ventures.

Puranik noted that during the oil price downturn between 2014 and 2017, many exploration and production companies were able to receive refinancing from investors for about six to seven years amid hopes of price recovery.

But oil prices have not risen sufficiently while the debt raised by operators is nearing its repayment period in the next two years, according to the analyst.

“This is raising alarms across the global oil and gas industry, and influencing deal activity,” he added.

“Many companies are starting to show capital prudence, and are resisting from making rash acquisitions.

“A classic example of this change of approach was Chevron, which stayed away from starting a bidding war with Occidental Petroleum over Anadarko Petroleum.”

Divestment appeared as a prominent global trend among several oil and gas companies worldwide during 2019.

Throughout the year, companies focused on selling assets to exit from non-profitable ventures or weak competitive positions in the market.

This is likely to enable companies to focus on core businesses and reduce debt levels, according to GlobalData’s report, titled M&A in Oil and Gas – 2020.

Puranik said oil and gas companies have focused recently on prioritising their areas of operations more on markets closer to their traditional bases.

He added: “This is why we are likely to see the UK or European operators acquiring assets in the North Sea, or US-based companies and oil majors targeting independent shale drillers.”

Why oil and gas firms are divesting in assets

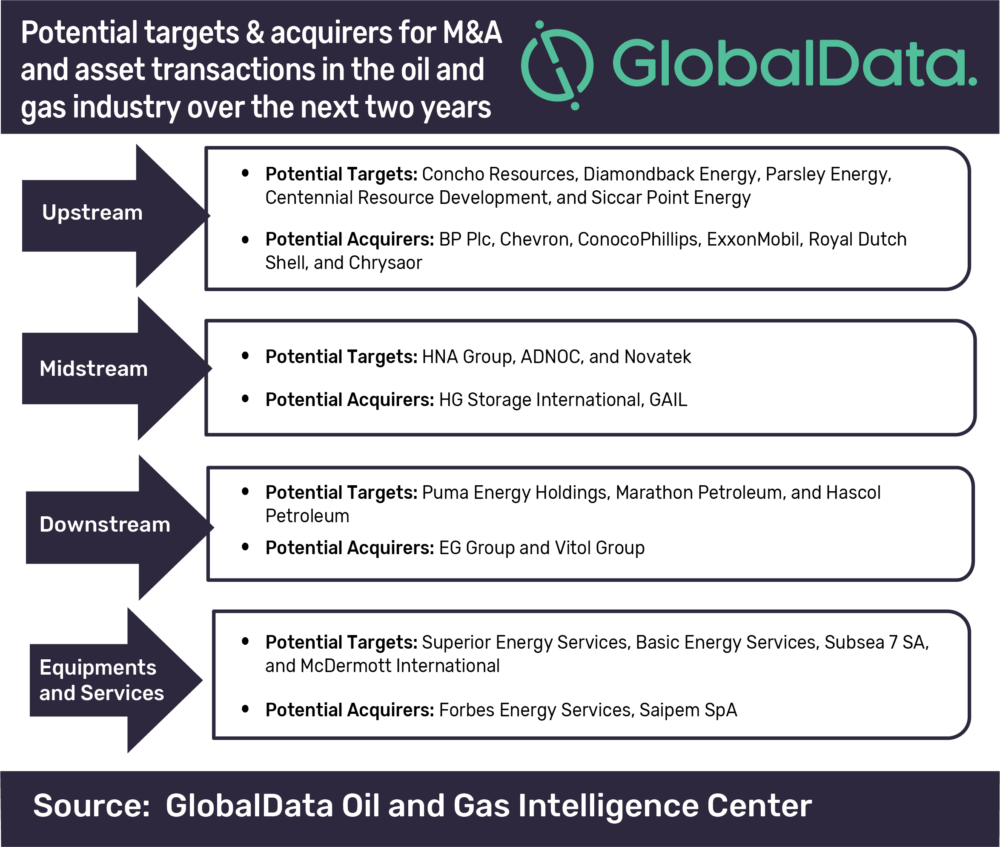

GlobalData’s research identifies oil and gas firms that are likely to offer either part of or their entire company for sale in the coming two years.

It also includes independent shale drillers, such as Concho Resources, Diamondback Energy and Parsley Energy, as well as midstream and downstream operators, such as HNA Group, Novatek Puma Energy, and Hascol Petroleum which may divest a partial stake in the near future.

According to the report, environmental concerns and stricter norms imposed by authorities are restricting the carbon-intensive industry from operating in specific geographic areas.

As a result, in 2019, companies announced their exits from projects that generate high-carbon emissions or are located in ecologically sensitive areas.

Oil and gas giant BP announced the sale of its entire business in Alaska to US firm Hilcorp Energy for a total consideration of $5.6bn.

The deal included the sale of BP’s upstream portfolio of the Prudhoe Bay oil fields in the Alaska North Slope and associated midstream assets in the region.

Puranik said this divestment is likely to “help BP in reducing its net methane emissions from global operations”.