ExPPERTS Europe is an annual meeting (ExPPERTS standing for Exploring Power Plant Emissions Reduction – Technologies and Strategies)*, in its 11th year, which is very well attended by industry and utilities – over 90 registered delegates, mainly from Europe and with a good representation from countries such as Croatia and Bulgaria.

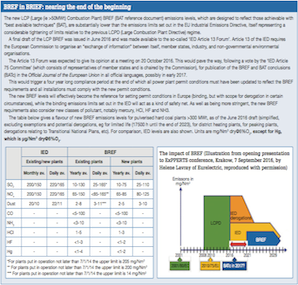

The first morning of the meeting concentrated on emerging European legislation, especially the new BAT (best available technology) requirements. After five years of work, the BREFs (BAT reference documents) are concluded which means that new limits are imminent under new permits. The limits in the new BREF will come into play in 2021 and will then tighten again in 2029.

Between 2005 and 2013 emissions in the EU from the power sector dropped significantly (SO by 71%, NO by 38% and PM2.5 by 38%) whilst generation remained stable (-1%). A total of 115 GW of older plants closed between 2008 and 2016 and more closures are expected, the aim being to decarbonise the power production sector by 2050. But the load factor of existing plants is dropping and wholesale electricity prices have fallen to levels that do not reflect the generation costs, and therefore the economics of fossil fuel plants are more challenging whilst those same plants are still very much required to provide baseload power (see also my recent report Levelling the intermittency of renewables with coal, CCC/268, and a new IEA CCC report coming soon from Hermine Nalbandian-Sugden).

Coal plants are therefore facing tightening legislation, increased costs and the knowledge that they are to be phased out by 2050. This makes investment in any new control technologies to comply with more stringent limits less profitable – operators must estimate the remaining lifetime of the plant and potential income against retrofitting costs. Costs are high – the estimate for Poland’s compliance is >€2billion.

Despite emissions of pollutants such as SO2 and NOx peaking during the fossil fuel fired 20th century, emissions levels are now back to as low if not lower than they were in 1920. However, air quality problems still exist in the EU. The European Commission aims to reduce the health impact of air pollution by 50% by 2030 compared with 2005.

The main issue is PM2.5 which is a combination of primary and secondary particulates from a combination of sources (see report by Xing Zhang of the IEA Clean Coal Centre on PM2.5 (CCC/267)). Therefore, to reduce emissions of PM2.5 requires a reduction in emissions of pretty much all the major pollutants.

The new National Emission Ceiling Directive(NECD)targetsincludeupdated member state targets for each individual pollutant (SO2, NOx, NMVOC, NH3 and PM2.5, the latter being a new addition) which are legally binding for 2020 and 2030, with an intermediate non-binding target for 2025.

Although the NECD only specifies reduction targets for countries and does not dictate how these reductions should be achieved, it is apparent that the energy sector is expected to provide a significant proportion of the reductions required, especially for SO2. The transport sector will have the major challenge for NOx. There are some mechanisms for flexibility included within the NECD such as to allow for challenging winters and the adjustment of non-representative emission factors. There are also derogations permissible for compliance which may risk the security of supply or energy poverty. There is in addition an option to exceed emissions for one pollutant where the cost-effectiveness is not valid as long as a second pollutant is reduced at a higher rate as a form of compensation. There is a table provided to define equivalence factors for trading pollutants in this way. For example, VOC have an equivalence factor of 0.01 with PM2.5 – so if 1.0 t of PM2.5 is not reduced then 0.01 t of VOC reduction is required instead.

Although the energy sector is not targeted directly, it is likely that other sectors (transport, agriculture, domestic heating and so on) will underperform in terms of emissions reduction thus increasing the pressure on the energy sector to make up the required reduction.

A speaker from Polish heat and power provider PGNiG Termika had some interesting insights on compliance issues, looking at the various risks in the decision making process for plants to remain in operation as legislation tightens. This included everything from energy efficiency and market demand through to depreciation of assets and security of supply. This means working through a decision strategy such as the following:

- Prognosis of the prospective market demand for electricity.

- Type and size of facility and production profile.

- Environmental obligations.

- Emissions abatement technique.

Following this, there is then the consideration of derogations or even indefinite exemption. The latter is provided in the case of challenging technology and economic factors but is not completely indefinite, only within the term of the permit and must be reconsidered each time the permit is re-issued. Perhaps the main point raised was the fact that plant operators and regulators face major problems with trying to operate plants and plan for the future whilst new directives evolve slowly in often a changeable and unpredictable manner. For example, although the new emission limits for mercury under the new BREFs have been being discussed for around five years, it is only in the last year that it has become clear how tight these emission limits may actually be and, even then, the final emission limit will ultimately be defined within the plant specific permit and may therefore by subject to further requirements.

The IED is currently UK law and the new NECD will be transposed before Brexit and therefore, in the near term, compliance continues in a business as usual way. The aim of the current UK government to phase out the use of coal for power generation by 2025 will mean that emissions will be reduced significantly within the next decade and compliance with most EU directives should not be an issue. It wasn’t mentioned, but security of electricity supply during and following this coal phase out period could be a challenge.

A comparison of the IED implantation plans for Germany and the UK showed that the UK does not specify CO limits (Germany does) and the UK does not specify SCR as obligatory (with only one SCR system installed to date, that at Ratcliffe). In fact, the Aberthaw coal-fired power plant currently has a NOx emission level which is several times higher than other UK plants as it has accumulated allowances under the UK’s transitional action plan, allowing it to avoid installing SCR (and is the subject of infraction proceedings against the UK government in relation to the permit granted).

The tightening of emission limits under the new BREFs, especially for mercury, will pose an implementation problem for many operators. Low CAPEX options will be preferred due to the limited remaining payback opportunities (before the move away from coal-fired generation completely). “Extremely” competitive capacity auctions also challenge the economics of retrofits. Flexibilityincoalplantswas“requiredbut not rewarded” and large clean plants lose out to smaller, dirtier, and less efficient units.

The meeting then broke out into panel debates and roundtable discussions which allowed delegates to discuss issues and challenges in a more sociable and less public manner – this was a good opportunity to chat to plant operators and regulators in different regions. For example, delegates from Croatia and Bulgaria gave great personal insights into the challenges faced by these regions to comply with EU regulations. Plans to build a new coal plant in Croatia have been halted and so further gas fired combined heat and power systems are planned instead. Croatia obtains the majority of its power from oil and gas fired plants, but does require some energy from a shared coal plant in Slovenia and from coal units in Bosnia and Herzegovina. Since the latter is not an EU member state, this means that the coal power comes from a plant which produces more emissions than it would be allowed if it were in Croatia. This raised the valid point that, as countries such as Germany and the UK move rapidly towards renewables, the situation often arises that power needed to meet grid requirements is produced from neighbouring countries with lower compliance requirements and thus actually mask emissions which arise due to demands in these countries.

The remaining presentations at the meeting were more technical, focussing on emissions control and water control maintenance and many veered towards being somewhat commercial/sales-pitch talks, but with enough data and information included so as still to be of interest to regulators and utilities who may soon be actively looking for such systems to comply with the new emissions requirements.

* Organised by Arena International, an affiliate of Modern Power Systems

Dr Lesley Sloss, Principal Environmental Consultant, IEA Clean Coal Centre (UK); Lead, UNEP Mercury Coal Partnership