The 2014 edition of the International Energy Agency’s World Energy Outlook* is a detailed analysis of global energy trends to 2040 based on various possible scenarios. It is the first time the IEA’s projections have looked so far ahead and the picture it paints is one of an increasingly stressed world energy system.

The global energy system, says the IEA, is in danger of falling short of the hopes and expectations placed upon it. Turmoil in parts of the Middle East – which remains the only large source of low-cost oil – has rarely been greater since the oil crises of the 1970s. Conflict between Russia and Ukraine has re-ignited concerns about gas security. Nuclear power, which for some countries plays a strategic role in energy security (a topic examined in depth in WEO-2014), faces an uncertain future. Electricity remains inaccessible to many people, and the region comes under special focus in WEO-2014.

The point of departure for the climate negotiations, due to reach a climax in Paris in 2015, is not encouraging: a continued rise in global greenhouse-gas emissions and stifling air pollution in many of the world’s fast-growing cities.

Certain key issues are identified.

- Geopolitical & market uncertainties are set to propel energy security high up the global energy agenda.

- Volatility in the Middle East raises short-term doubts on investment and suggests difficulties for the future oil supply

- Nuclear power can play a role in energy security & carbon abatement – but financing & public concerns are key issues.

- Mixed signals in the run-up to the crucial climate summit in Paris in 2015. Global CO2 emissions are still rising, with most emitters on an upward path, but at $550 billion, fossil fuel subsidies are at a level over four times that applied to renewables. How close is the world to using up the available ‘carbon budget’, which cannot be exceeded if global warming is to be contained?

And the IEA issues a stark warning. Without clear direction from the 2015 Paris conference, the world is set for warming well beyond the 2°C goal, and far-sighted government policies will be essential to steering the global energy system on to a safer course. If these signs of stress are ignored, says the IEA, the energy sector will be unable to tackle longer-term weaknesses before they reach breaking point.

Main scenario

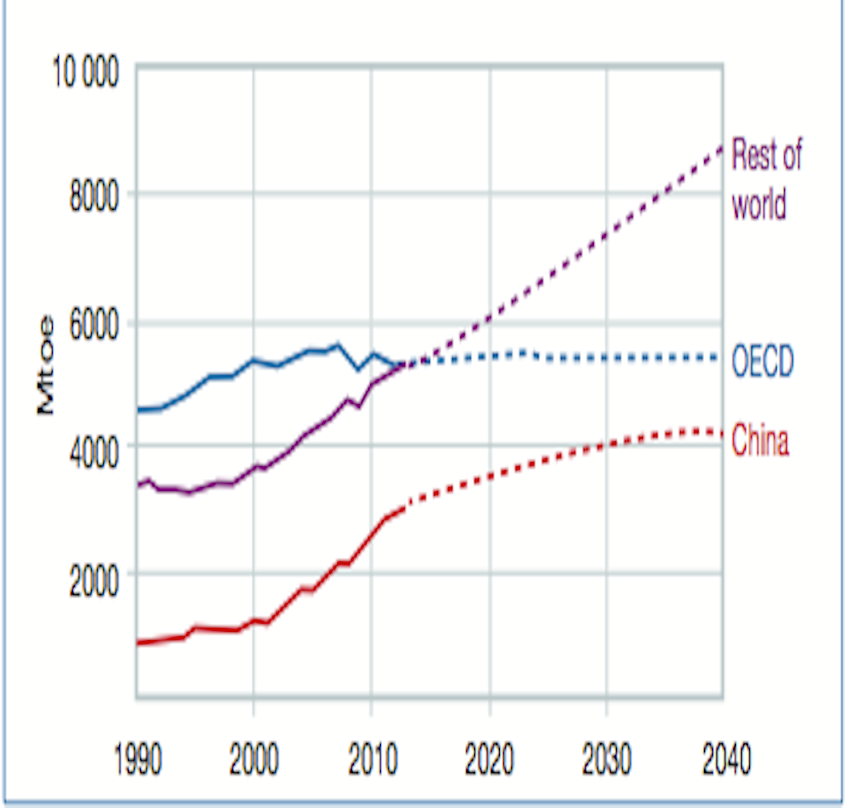

In the IEA’s central scenario, world primary energy demand rises by 37% to 2040, but this increase would be even greater without the braking effect of efficiency measures, which are playing an important part in holding back global demand growth. This scenario shows that world demand for coal and oil will flatten out by 2040, although, for both fuels, this global outcome is a result of very different trends across countries. At the same time, renewable energy technologies gain ground rapidly, helped by falling costs and subsidies (estimated at $120 billion in 2013). By 2040, world energy supply is divided into four almost equal components – low-carbon sources (nuclear and renewables), oil, natural gas and coal.

Rapid population and economic growth is driving up electricity demand in Asia. The IEA forecasts generation capacity in Southeast Asia to triple between 2011 and 2035, still largely fuelled by coal. This view is backed by the Asian Development Bank which predicts that demand in Asia-Pacific will increase by 52.8% from 2010 to 2035.

Nuclear power

In an in-depth focus on nuclear power, WEO-2014 sees installed capacity grow by 60% to 2040 in the central scenario, with the increase concentrated heavily in only four countries (China, India, Korea and Russia). Despite this, the share of nuclear power in the global power mix remains well below its historic peak. Nuclear power plays an important strategic role in enhancing energy security for some countries. It also avoids almost four years’ worth of global energy- related carbon-dioxide (CO2) emissions by 2040. However, nuclear power faces major challenges in competitive markets where there are significant market and regulatory risks, and public acceptance remains a critical issue worldwide. Many countries must also make important decisions regarding the almost 200 nuclear reactors due to be retired by 2040, and how to manage the growing volumes of spent nuclear fuel in the absence of permanent disposal facilities.

Role of renewables

Renewables are expected to account for nearly half of the global increase in power generation to 2040, and overtake coal as the leading source of electricity. Wind power accounts for the largest share of growth in renewables-based generation, followed by hydropower and solar technologies. However, as the share of wind and solar PV in the world’s power mix quadruples, their integration becomes more challenging both from a technical and market perspective.

Oil and gas

World oil supply rises to 104 million barrels per day (mb/d) in 2040, but hinges critically on investments in the Middle East. As tight oil output in the USA levels off, and non-OPEC supply falls back in the 2020s, the Middle East becomes the major source of supply growth. Growth in world oil demand slows to a near halt by 2040: demand in many of today’s largest consumers either already being in long- term decline by 2040 (the United States, European Union and Japan) or having essentially reached a plateau (China, Russia and Brazil). China overtakes the United States as the largest oil consumer around 2030 but, as its demand growth slows, India emerges as a key driver of growth, as do sub-Saharan Africa, the Middle East and SE Asia.

“A well-supplied oil market in the short-term should not disguise the challenges that lie ahead, as the world is set to rely more heavily on a relatively small number of producing countries," said IEA chief economist Fatih Birol. "The apparent breathing space provided by rising output in the Americas over the next decade provides little reassurance, given the long lead times of new upstream projects."

Demand for gas is more than 50% higher in 2040, and it is the only fossil fuel still growing significantly at that time. The USA remains the largest global gas producer, although production levels off in the late 2030s as shale gas output starts to recede. East Africa emerges alongside Qatar, Australia and North America as an important source of LNG, which is an increasingly important tool for gas security. A key uncertainty for gas outside North America is whether it can be made available at prices low enough to be attractive for consumers and yet high enough to incentivise large investments in supply.

Coal

While coal is abundant and its supply relatively secure, its future use is constrained by measures to improve efficiency, tackle local pollution and reduce CO2 emissions. Coal demand is 15% higher in 2040 but growth slows to a near halt in the 2020s. Regional trends vary, with demand reaching a peak in China, dropping by one-third in the United States, but continuing to grow in India.

In the medium term the coal burn will continue to increase. An IEA report, its annual Medium-Term Coal Market Report released in December finds that global demand over the next five years will break the 9-billion-tonne level by 2019. It notes that despite China’s efforts to moderate its coal consumption, it will still account for three-fifths of demand growth during the outlook period. Moreover, China will be joined by India, ASEAN countries and other countries in Asia as the main engines of growth in coal consumption, offsetting declines in Europe and the United States.

“We have heard many pledges and policies aimed at mitigating climate change, but over the next five years they will mostly fail to arrest the growth in coal demand," said IEA executive director Maria van der Hoeven. "Although the contribution that coal makes to energy security and access to energy is undeniable, I must emphasise once again that coal use in its current form is simply unsustainable. For this to change, we need to radically accelerate deployment of carbon capture and sequestration, and high-efficiency coal plants".

Energy poverty

The global energy system continues to face a major energy poverty crisis. In sub-Saharan Africa two out of every three people have no access to electricity, and this is acting as a severe constraint on economic and social development. Meanwhile, fossil-fuel consumption subsidies (estimated at $550 billion in 2013), often intended to help increase energy access, are failing to help those that most need it, but curtailing investment in efficiency and renewables.

CO2 emissions

A critical sign of stress is the failure to transform the energy system quickly enough to curtail the rise in CO2 emissions, which will grow by 20% to 2040 and set the world on a path to a long-term global temperature increase of over 2°C. In the IEA’s central scenario, the entire carbon budget allowed under a 2°C climate trajectory is consumed by 2040, highlighting the need for a comprehensive and ambitious agreement at the 2015 COP21 meeting in Paris.

*World Energy Outlook 2014 is on sale at the IEA bookshop

(Originally published in MPS January 2015)