The US nuclear power industry geared up a decade ago for a nuclear renaissance that did not happen and is not likely to happen. If things were not bad enough, some existing US merchant nuclear projects face economic pressure, with some of these units retiring early. By Ed Kee

The US Energy Policy Act of 2005 included loan guarantees and other incentives aimed at starting a new round of nuclear build. The US Nuclear Regulatory Commission (NRC) licensing approach had been revised, with the aim of making new nuclear plant licensing less difficult and less risky for project sponsors.

In 2002, the US Department of Energy started the Nuclear Power 2010 Program. NP 2010 included public/private partnerships to develop advanced reactor designs, explore sites for new nuclear power plants, and demonstrate the new US NRC "one-step" nuclear power plant licensing process. Programme goals included orders for new nuclear power plants by 2005 and operational new nuclear power plants by 2010. The goal for operational nuclear power plants was not met, but NP 2010 led to the filing of more than 15 NRC licence applications for new nuclear power plants.

The US nuclear renaissance was expected to be a wave of new nuclear build. This would start with safer and more economic standardized reactor designs built in the US. The hope was that the US new nuclear build would lead to a new wave of nuclear build outside the country.

Today, only five reactors are under construction in the US. Four of these reactors (the Vogtle and Summer projects) use the same Westinghouse AP1000 standard reactor design. The fifth is a 1970s reactor design at Watts Bar 2, where a project put on hold decades ago is being completed. This is far short of the number of new nuclear projects expected in 2005.

Aside from these projects, no new US nuclear projects are expected to start construction in the next decade or longer. Many of the NRC applications have been suspended or withdrawn, but most recent US NRC COL application status table shows that there are eight applications that are under review.

A discussion of these eight projects shows that they are unlikely to start construction soon. Most of these applications are proceeding as a means of keeping the option to build alive.

As it became clear that the nuclear renaissance was not going to happen, the US nuclear industry focused on finding markets outside the US. Non-US reactor vendors that had been behind several new nuclear projects have largely abandoned the US market.

Threats to existing fleet

The lack of new nuclear projects in the US is bad for the nuclear industry, but many of these companies provide nuclear fuel, products, and services to the large US operating nuclear power fleet.

The US has 100 operating power reactors, more than any other country. Many of these reactors have received approval from the US NRC to operate for 20 years past the end of their original 40-year operating licences. The US nuclear power industry has an excellent safety and operating record, with annual average capacity factors at or above 90% since 2000. In 2013, the share of total US electricity supplied by nuclear was 19.4%, down only slightly from the all-time high of 20.6% in 2001.

Despite this excellent performance, several operating nuclear power plants in the US permanently closed in 2013 and more are at risk.

The Crystal River and San Onofre Nuclear Generating Station plants were retired early in 2013 due to maintenance issues.

The Kewaunee nuclear power plant was retired early in 2013 due to economic issues. The Vermont Yankee nuclear power plant will be retired early at the end of 2014 for economic reasons. Both of these units received NRC approval to operate for 20 years past the expiration of the original operating licence, but decided that continued operation would not be profitable.

More existing nuclear power plants face economic issues similar to those that led to the early retirement of the Kewaunee and Vermont Yankee plants.

The US electricity industry is behind both the missing nuclear renaissance and recent economic early retirements.

The American electricity industry

The US electricity industry has several different electricity industry structures and company types.

Public power

The US electricity industry has many municipal, government, and cooperative utilities. These public power utilities have several common features, including exemption from income taxes. These public power utilities typically make long-term power plant investments and enter into long-term power purchase agreements to minimise the long-term total cost of electricity to their members or customers.

Regulated

Some parts of the US have retained the traditional regulated investor-owned utility approach, with vertically integrated investor-owned utilities that are overseen by state utility commissions. Investor-owned regulated utilities coexist with public power utilities and often join with them in power plant projects.

Regulated utilities undertake long-term planning and investment aimed at minimising the long-run total cost of electricity to consumers. This total cost is composed of costs of long-term assets like power plants and transmission lines and short-run operating costs. This long-term focus is supported by, or even imposed by, state utility regulators. In some states, the regulator allows the recovery of costs associated with the development of a nuclear generation option. This may include site studies and NRC licence applications as discussed above. A firm commitment to build will only come after an Integrated Resource Plan including the nuclear power plant option is approved. Georgia and South Carolina established a regulatory process for new nuclear power plants and engaged in a detailed regulatory review and approval process for the Vogtle and Summer units that are now under construction.

Electricity markets

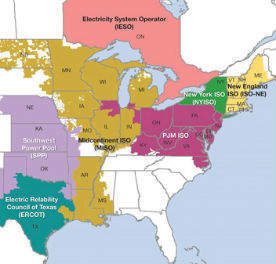

In some US regions, the electricity industry was restructured and regional electricity markets were put in place. The US electricity markets are based on regional transmission organisations, pre-reform regional power pools, or electricity coordination regions. There are several different electricity markets in the US, each with different rules and approaches, all overseen by the US Federal Energy Regulatory Commission (FERC).

Figure 1 shows the North American electricity market regions. The white space represents regions with other electricity industry structures.

In these electricity markets, the primary organising principle is minimising short-term market prices by the short-run dispatch of existing power plants. These markets are not focused on long-term planning and investment in generation. Instead, there is an expectation that electricity market spot prices would provide price signals for long-term market-based generation investment. This has not worked well.

Power plant investments in these electricity markets are focused on minimising risk and maximising return to power plant investors, not on minimising long-run total electricity costs to end users.

Existing merchant nuclear

None of the proposed new merchant nuclear projects in the US is moving ahead. However, a number of merchant nuclear projects were created as a part of US electricity industry restructuring. These merchant nuclear plants, built under the earlier regulated utility industry structure, were divested as a part of electricity industry reform.

The divested nuclear power plants were typically bundled with a power purchase agreement (PPA) with the former utility owner that remained a regulated retail electricity provider. The PPAs typically covered the remainder of the original licensed life of the nuclear project. These PPAs (before they expired) meant that the new merchant nuclear power plants were less risky and had a more certain value.

As these PPAs expired, some quite recently, the nuclear power plants were transformed into pure merchant generators that depend on the electricity market for revenue. The Kewaunee and Vermont Yankee plants that have been (or will soon be) retired early due to economic issues are part of the US merchant nuclear fleet with PPAs that were expired or that were due to expire.

Both these plants sought to negotiate new PPAs, but in an electricity market that was very different from the market a decade earlier.

Shift away from nuclear power

US electricity fundamentals became less favourable for nuclear power projects because of low natural gas prices, low demand growth, and increased renewable generation.

Low natural gas prices

The US electricity industry has been transformed by non-conventional (shale) natural gas production that provide abundant low-cost natural gas for generation fuel. The US DOE EIA reference case natural gas prices delivered to electric power users is less than $8 per thousand cubic feet in 2012 US Dollars until the end of the forecast period in 2040.

In most US electricity markets, power plants using natural gas as fuel are on the margin and set electricity market spot prices in many hours of the year. Lower natural gas prices results in lower electricity market prices. Lower electricity market prices mean lower revenues for merchant nuclear generators that sell into the electricity markets. An example is the MISO market. Figure 2 (below) shows how MISO prices have moved lower since 2007, tracking natural gas prices.

The US is expected to have relatively low natural gas prices for more than 30 years. This means that electricity market revenue for existing and new merchant nuclear power projects will be low for a long time. The projected low electricity market prices also stopped the development of new merchant nuclear projects. The current and projected low electricity market prices are a primary reason that existing merchant nuclear projects have retired early and that others are threatened.

These low natural gas prices have also had an impact on regulated regions. Utility regulators require utilities to undertake an integrated resource planning (IRP) process to decide on the amount, type, and timing of new capacity investments. Since about 2010, the results of these IRP processes have been dominated by power plants using natural gas fuel.

Low demand growth

US electricity growth has been slow, with 2013 total consumption about 3% lower than 2005 total consumption. The US EIA predicts that total electricity use will grow at a low rate (about 0.8% per year) until 2040.

Increased renewable generation

The US has encouraged new renewable generation projects that include wind and solar (but not nuclear power). Significant financial incentives were provided to US renewable energy projects through federal income tax credits and state-level renewable portfolio requirements.

With little US electricity consumption or demand growth, incentives for renewable generation resulted in new capacity and electricity production that reduced electricity spot market prices in electricity markets and reduced the need for new power plants in regulated regions.

While an increase in intermittent renewable generation leads to an increased need for fast-response generation to maintain system reliability, this fast-response generation is usually provided by natural gas fired generation (not nuclear).

Making matters worse, US federal income tax credits for renewable projects are structured as production tax credits (PTCs). The financial benefit of a PTC is linked to actual physical energy production of a renewable facility. PTC subsidies provide revenue that is unlinked from electricity market revenues, but linked to renewable project operation in the electricity market.

PTCs create an incentive for a renewable generator to bid at negative prices. This is a rational bidding strategy created by the out-of-market revenue from production tax credits. Some state-level renewable incentives are also outside the electricity market but linked to actual physical output, providing similar economic incentives for renewable projects to bid at negative prices.

Negative bidding by renewable projects distorts electricity market prices. In Texas and other parts of the US, there are periods of negative electricity market spot prices when demand is low and wind generator output is high.

Low and negative electricity market spot prices mean lower revenues (or even losses) for a nuclear unit that is operating at maximum output at all times between refuelling outages.

Impact in different markets

Worsened electricity fundamentals have an impact on all nuclear power plants, but this differs by type of project and the electricity industry structure.

A regulated or public power utility project that is started will typically continue despite market changes after the project starts. Unlike a regulated project, a new merchant generation project may be more closely linked to market conditions. Three examples:

- Vogtle 3&4 (AP1000) – This new nuclear project is in the regulated utility state of Georgia. The plant is owned by Georgia Power Company (a regulated utility that is a part of the larger multi-state Southern Company), Oglethorpe Power (a generation and transmission cooperative), the Municipal Electricity Authority of Georgia (an entity with members that are municipal/city utilities in Georgia), and the city of Dalton, Georgia. All the owners are either government or regulated utilities. The Vogtle 3&4 project was approved by the Georgia Public Service Commission in about 2007 after an IRP process. This approval resulted in a commitment to invest by the regulated utility owner and the regulator. The regulatory approval ensures that the regulated utility gets a return from its investment.The Vogtle 3&4 project is under construction. Some of the project owners received US DOE loan guarantees on favourable terms. After the Vogtle 3&4 project was approved, subsequent Georgia IRP analyses have selected natural gas fired generation rather than additional new nuclear power.

- Calvert Cliffs 3 (US EPR) – This proposed new merchant nuclear project is located in Maryland near Washington DC and would operate in the US PJM electricity market. The Calvert Cliffs 3 project might have been a reasonable investment for a merchant generation company if the electricity fundamentals prior to 2005 had remained in place and the project had been able to arrange financing using the US DOE loan guarantee programme. As electricity fundamentals moved against the project and the loan guarantee financing arrangements were not favourable, the project’s financial situation became difficult. The Calvert Cliffs 3 project is, at best, on hold.

- Watts Bar 2 – The Tennessee Valley authority is a public power utility, a federal power marketing agency and developer of hydroelectric facilities that moved into nuclear power. It is a government utility, with no profits and no shareholders. TVA has recently embarked on an effort to complete construction at the Watts Bar 2 project. This project started construction in the 1970s and was put on hold. The Watts Bar 2 project is expected to be operational in 2015. TVA’s resource plans consider natural gas alternatives, but have the ability to reflect a range or objectives beyond short-term cost. Watts Bar 2 is under construction.

The market conditions that will result in new nuclear power plant investments differ by industry structure. A merchant nuclear project might need high electricity market prices that are projected to continue for several decades to justify an investment, especially with low expectations for carbon credit revenue. The price expectations might be lower for a new nuclear power project built by a regulated or government utility, as state utility regulators or government utility owners place a value on nuclear power plant attributes such as low carbon emissions, stable/less-volatile fuel cost, and reliable operation.

Hope for a US nuclear revival

The US nuclear power industry will likely face unfavourable electricity industry conditions for another 20 years or longer. Some efforts have been made to provide additional financial incentives to US nuclear power. As electricity market conditions become less favourable, other measures such as short-term capacity markets or carbon tax proposals will be less effective in helping existing or new projects.

Some US states have tried to take action to address the failure of electricity markets to deliver new power plant investments. New Jersey and Maryland, both in the PJM electricity market, required that regulated retail utilities enter into long-term contracts intended to support power-plant investments. New Jersey used 15-year capacity contracts and Maryland used 20-year contracts for differences. These programmes might have been used for nuclear projects, but were not limited to nuclear. The New Jersey and Maryland initiatives were challenged in court. In both cases, courts ruled that the state initiatives were not valid because the US federal government has exclusive jurisdiction over interstate electricity, wholesale electricity markets, and wholesale electricity transactions.

There are negotiations in Illinois and other states about state-level actions to provide more revenue for merchant nuclear plants facing economic issues.

The recent US Environmental Protection Agency (EPA) proposed Clean Power Plan would establish emission guidelines for US states to follow in developing plans to address greenhouse gas emissions from existing fossil fuel-fired electric generating units. This would include state-specific goals for carbon dioxide emissions from the power sector, as well as guidelines for states to follow in developing plans to achieve the state-specific goals. While this proposal lays out state-specific CO2 goals that each state is required to meet, it does not prescribe how a state should meet its goal.

The EPA approach relies on the best system of emission reduction. To translate BSER into state-level goals, the EPA has grouped measures into four main categories, or ‘building blocks’ with state goals for each building block. The building blocks are:

- Heat rate improvements at existing electricity generation units

- Replacing generation from high-carbon intensity generating units (such as coal) with generation from lower-carbon intensity options such as natural gas combined cycle units

- Expanding low- or zero-carbon generation

- Expanding demand-side energy efficiency efforts

Block 3 includes nuclear power plants, but only 6% of existing nuclear generation is included in the calculation. This is based on the amount of existing US nuclear capacity that is at risk of economic early retirement according to a US DOE analysis. Some claim that the EPA state goal calculation is flawed in its treatment of nuclear generation. The debate over this proposed rule may result in changes, but current expectations are that this approach will provide little or no benefits to any particular existing nuclear project.

The author has proposed that a US government programme be established to enter into contracts for difference with threatened merchant nuclear plants to avoid early retirement (see http://tinyurl.com/ob87jwl).

While some efforts may be able to save existing US merchant nuclear projects facing financial issues, this is far from certain.

It is even less likely that any politically-feasible approach will be able to provide the incentives needed for new US merchant nuclear power plants.

What can the US industry do?

The US nuclear industry will not see another new US nuclear project in a long time and may see a further drop in operating units in the US. The US nuclear power industry should look outside the US for new business.

While efforts to move into the international market have been made, US company sales outside the US are also falling short of the expectations of a decade earlier.

US reactor vendors have had little success selling reactors in competition with government-owned reactor vendors. The US nuclear industry has limited participation in the growing number of new nuclear countries and projects outside the US.

The world market today has government reactor vendors that bring significant recent experience, proven advanced-reactor designs, the ability to make commitments backed up by large governments, and the potential to act as lenders or equity owners.

US nuclear vendors must reconsider their traditional role as nuclear power plant vendors. Winning orders in the current global nuclear power market may require additional activities such as vendor financing or even vendors acting as owners and operators of new nuclear power plants.

About the author

Edward D. Kee is the owner and principal consultant at Nuclear Economics Consulting Group (NECG) and is an Affiliated Expert with NERA Economic Consulting; he is based in Washington DC.